The popular Green Day song titled “Wake Me Up When September Ends” feels quite appropriate given the recent market volatility. In fact, the S&P 500 has now dropped at least 3% for three of the past four weeks. As we’ve noted in this commentary, stocks tend to be quite volatile and potentially weak in September, and that is playing out once again in 2022.

- It’s been another volatile September. We’ve seen this before, and it may not be over yet.

- We expect there’s more room for interest rates to rise, especially if core inflation remains high.

- The Fed is likely to raise interest rates by 0.75% in September, but the key will be how far the Fed will go.

- Economic indicators, including retail sales, manufacturing, and unemployment claims, do not point toward a recession.

It isn’t all bad though. The last three months tend to do quite well in a midterm election year, so we are still optimistic an end-of-year rally is possible. One more positive is just how bad the action was on Tuesday. After the hotter-than-expected inflation data (more on that below), the S&P 500 fell 4.3% for the worst single day for stocks since June 2020. Along the way, less than 1% of the S&P 500 finished higher, one of the lowest readings in recent memory. This is the 20th time since 2000 that less than 1% of S&P 500 stocks closed higher on a single day. But only twice were stocks still down one year later, and the average return was a very solid 19.1%.

Not to be outdone, every stock in the Nasdaq 100 closed red on Tuesday, for only the 13th time in history and the first time since March 12, 2020. But looking back at the index one year after this rare event shows the Nasdaq 100 was higher every time and up 21.2% on average.

The bottom line is stocks will still be in a seasonally weak period for the next few weeks, so caution could be warranted. But the recent heavy selling is consistent with a market nearing bottom, and a strong year-end rally is still quite possible.

Interest Rates Could Keep Rising If Inflation Stays High

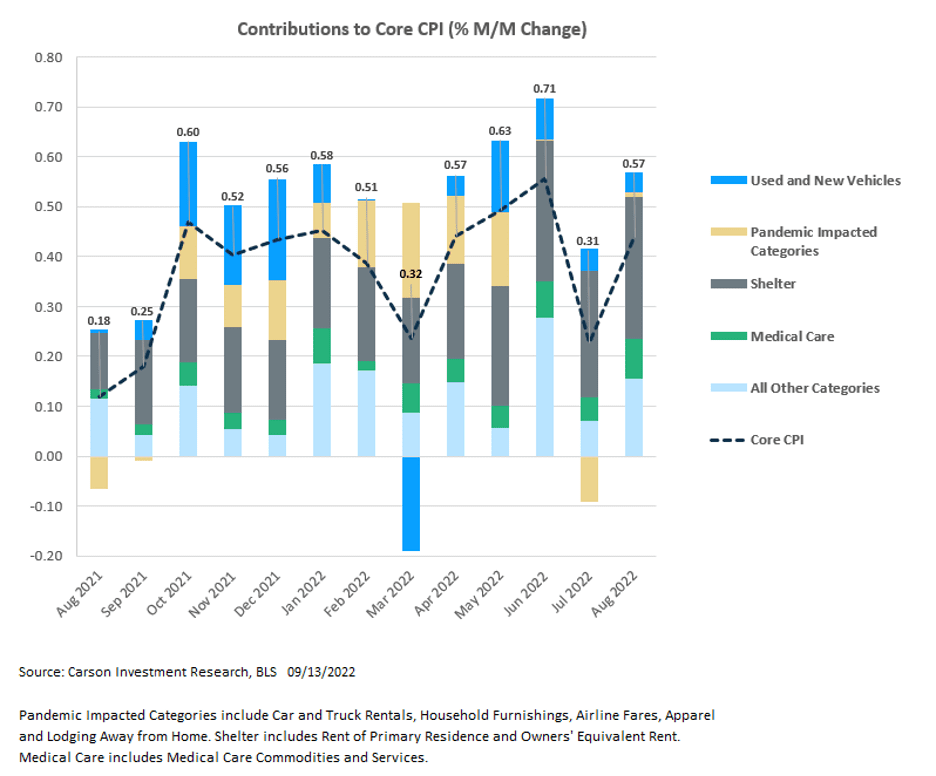

The August CPI report was not pretty. The headline number came in at 0.1%, pulled down by gas prices but higher than an expected -0.1% reading. The problem was core CPI, excluding food and energy, was 0.6%, twice what was expected. Tobacco, new vehicles, vehicle repairs, dental services, and hospital services all came in hotter than expected. Shelter costs continued to remain strong, while pandemic-impacted goods and services, including used/new cars, apparel, airfares, hotels, and furnishings, did not exert as much of a deflationary force as was expected by this time.

There were still some positives. For starters, CPI likely peaked in June at more than 9% year-over-year and fell to 8.3% in August. It should continue to trend lower. We have seen huge drops in prices paid in various manufacturing surveys, improvements in time to delivery, and imploding used car prices. All these factors will feed into the official inflation numbers over the next few months.

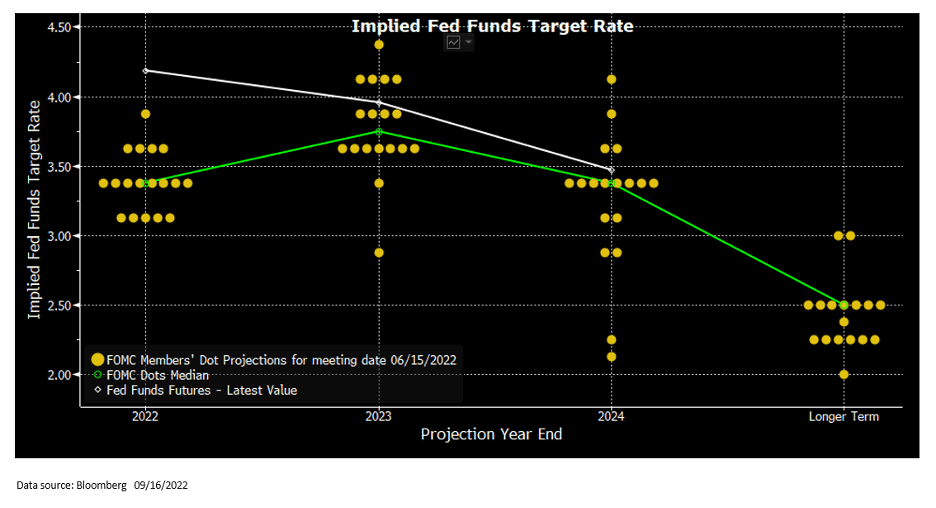

Nevertheless, markets were quick to react, as a hot inflation report led investors to expect the Fed to continue raising rates at a furious pace. Investors currently anticipate the federal funds rate to be raised as high as 4.2%. The white line in the chart below shows investor expectations for the fed funds rate, while the green line shows the median of the dots, which represent each Fed member’s estimate for where the policy rate will be in 2022 and beyond.

As you can see, the green line for 2022 is well below the white line (investor expectations). The Fed has a meeting this week, and we will be watching how much higher Fed members move their estimates and whether they match the market’s expectations. Our view is the green line will shift higher, close to 4% or more. That is why we’re still cautious on our outlook for interest rates. We believe there’s room for rates across the spectrum to rise — on the back of higher policy rates.

Short-term Treasury interest rates, which are a good approximation of monetary policy, have surged this year and are well above pre-crisis levels. After the August inflation report was released, one-year rates rose from 3.70% to 3.92%, while slightly longer-term five-year rates rose from 3.47% to 3.58%. So, they certainly are closer to where policy rates may get to but not quite there yet.

Still No Sign of Recession

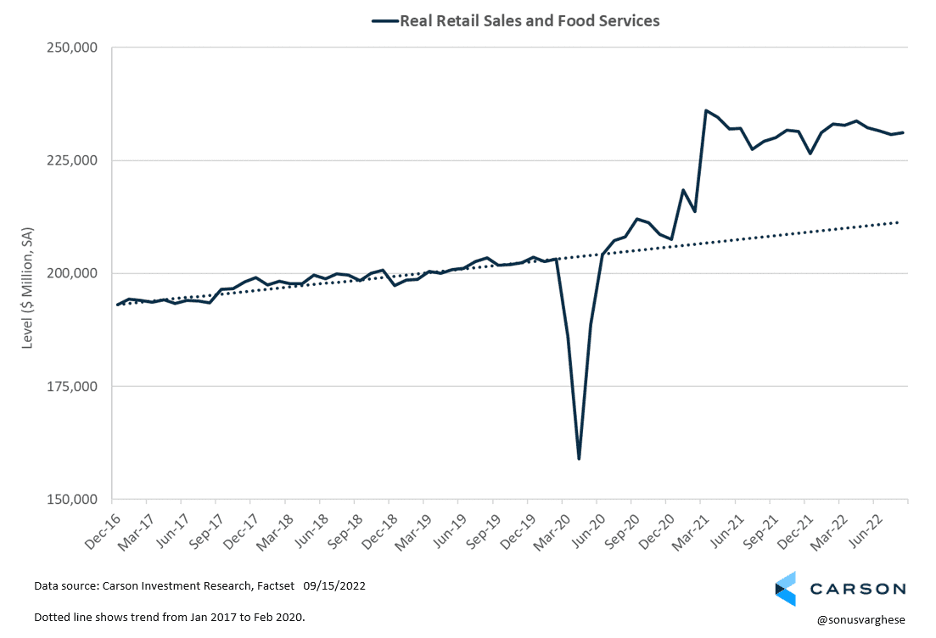

Data last week showed consumer spending remains solid, with retail sales rising 0.3% in August. This was mostly driven by auto sales, although spending was strong in various other sectors, including restaurants and building material and supply stores. The only drag was gasoline station purchases, where sales fell 4%, but that was because gas prices fell. If anything, we’re surprised at the strength of retail sales, which mostly comprise spending on goods, even as the country puts COVID in the rearview mirror. Real retail sales, which are adjusted for prices, rose 0.2% in August and are almost 10% above the pre-crisis trend, with no sign of slowdown yet.

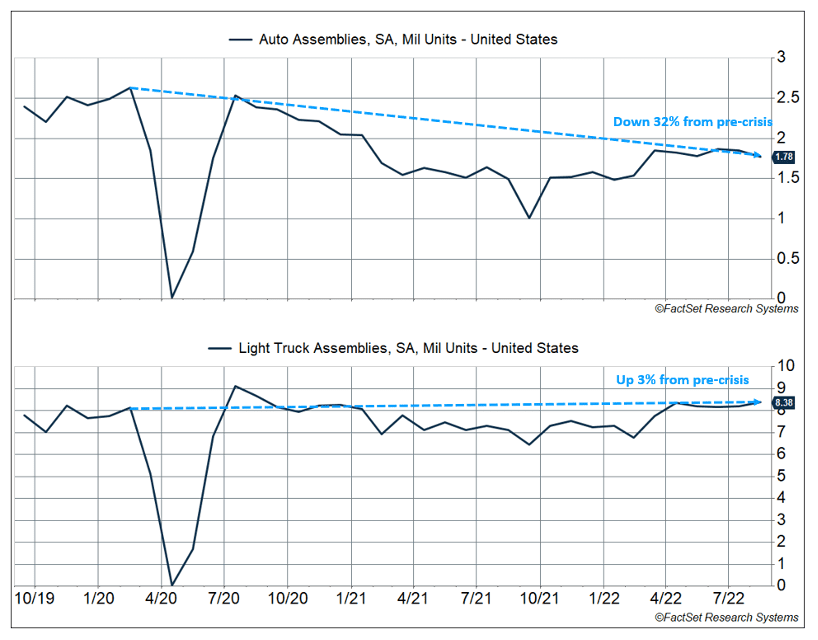

Industrial production did slow in August, falling 0.2%. However, this was because of a large pullback in electric power output. The all-important manufacturing sector saw production tick higher by 0.1%, and that overcame a 1.4% decline in motor vehicle and parts production. This is another puzzle for us — supply chains are clearly improving, but vehicle production remains below pre-pandemic levels. This is entirely because auto production is down about 32%, while light vehicle truck production (like SUVs) is back where it was. At the beginning of the year, we expected a pickup in auto production, providing more of a tailwind to the economy.

Finally, though certainly not the least important, unemployment claims continue to fall and remain well below pre-crisis levels. That means people getting laid off can find jobs quickly, without having to file for unemployment benefits — a sign of a very strong labor market. The downside is that increases the odds of the Fed continuing to raise interest rates to cool the economy down.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

Compliance Case # 01489423